众所周知,在REG的考试中,联邦税法的内容占到了60%以上的分值,而个人所得税更是重中之重。可以说,掌握个税知识是通过REG考试的充分必要条件。因此,在接下来的一段时间里,小编将带着大家一起深度的学习个人所得税体系。希望观者都可以从中有所收获。

回顾公式框架:

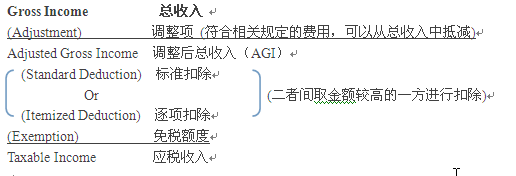

Gross Income 总收入

(Adjustment) 调整项 (符合相关规定的费用,可以从总收入中抵减)

Adjusted Gross Income 调整后总收入(AGI)

(Standard Deduction) 标准扣除

Or (二者间取金额较高的一方进行扣除)

(Itemized Deduction) 逐项扣除

(Exemption) 免税额度

Taxable Income 应税收入

首先一起来看一下Gross Income的计算。

Gross Income主要包括:劳务与工薪所得、股息所得、财产租赁所得、营业所得、资本利得、退休年金所得等。大家可以根据Form 1040个人所得税表的Income栏进行学习(Form 1040 Line7-22)下面简单的介绍一下Becker教材中提到的Gross Income的主要项目:

1. Compensation for services(包括工资薪酬,奖金小费,债务减免,廉价购买,guaranteed payment, 应税的福利收入)

| Item | Income |

| Property received | FMV |

| Bargain purchases | FMV-Price Paid |

| Guaranteed Payments/Money/Bonus | Value of Cash Received |

| Life insurance premiums | Exception: Group-term life insurance coverage of $50,000 or less. |

2. Interest Income(使用附表Schedule B,通常情况,利息收入都是应税的,除了以下的三类情况)

- Tax exempt interest income

State and local government bonds/obligations

Bonds of a U.S. possession

Series EE (U.S. savings bond)

3. Dividend Income(使用附表Schedule B,通常情况,股利收益都是应税的,但是有较低的税率0%,15%,20%)

- Taxable Dividend(Cash= amount received; Property = FMV)

- Tax-Free Distributions(Return of Capital, Stock Split, Stock Dividend,Life Insurance Dividend)

4. State and Local Tax Refunds(根据去年使用的是Itemized Deduction或者Standard Deduction,来确定州/地方的退税是否应税。)

5. Payments Pursuant to a Divorce

- Alimony/Spousal Support(Taxable)

- Child Support (Nontaxable)

- Property Settlement (Nontaxable)

6. Business Income Or Loss(使用附表Schedule C或者C-EZ来申报私营业主的相关营业收入)

7. Farming Income(使用附表Schedule F来申报农业收入)

8. Gains and Losses on Disposition of Property (变卖资产后的利得和损失)

9. IRA Income (根据IRA的类型,来确认个人退休账户收入是否应税。)

- Traditional IRA distributions: taxable as ordinary income

- Roth IRA distributions: nontaxable

- Nondeductible IRA distribution: Principal - Nontaxable

Accumulated earnings – Taxable

10. Annuities(年金投资的情况,投资资本返还的部分是非税的,超过投资资本的部分是应税的。)

- Non-taxable part = investment amount / recovering months number

- Taxable part = any amount exceeding the non-taxable part (monthly)

11. Rental/ passive activity Income(使用附表Schedule E来申报被动收入,包括租金,版税,合伙企业、LLC、S Corp的收入,遗产及信托的收入等)

12. Unemployment Compensation(失业补偿金,都是应税的。相对来说,worker’s compensation是非税的。)

13. Social Security Income(根据收入的不同,社会保障福利是部分应税的,至高是85%应税。)

- 如果AGI + 免税利息收入+ 50% of the social security benefits低于Single $25,000/MFJ $32,000,则全部社会保障福利都是非税的;

- 如果AGI + 免税利息收入+ 50% of the social security benefits收入高于Single $34,000/MFJ $44,000,则85%社会保障福利是应税的。)

14. Taxable Miscellaneous Income(其他应税的杂项收入)

- Prizes and Awards奖金和奖品

- Gambling Winnings赌博收入

- Business Recoveries为了补偿损失利润的收入

- Punitive Damages惩罚性赔偿

15. Partially Taxable Miscellaneous Items(部分应税的杂项收入,这里特指奖学金。如果满足一定要求,那么奖学金就是不应税的。如果没有满足要求,那么奖学金就可能算到应税收入中。)

To be continued…

![]()

了解详情30000元/4科