目标成本法在ACCA课程内容当中是较为重要的知识点,作为一个以培养高端财务人才为目标的ACCA考试,如何教会学员学会降低产品整个寿命周期内的总体成本,这自然是非常重要的。但什么是目标成本法?我们应该如何理解和掌握目标成本法呢?

目标成本法 Target Costing 定义:

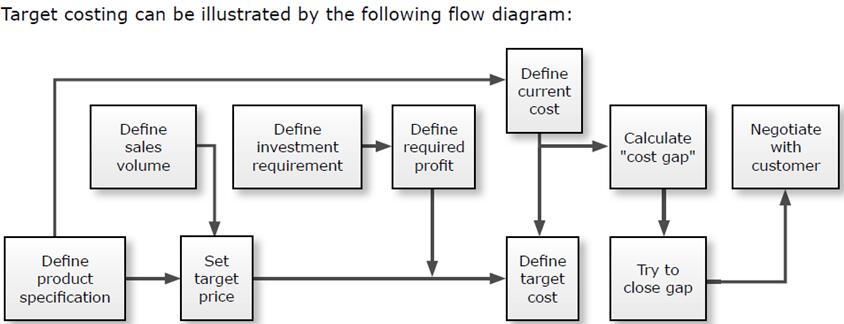

目标成本法是指以给定的竞争价格为基础,从而决定产品的成本,以保证实现预期的利润。目标成本法的核心工作是制定企业新产品的目标成本,并不断改进产品与工序设计,从而确保新产品的成本小于或等于目标成本。

Target costing is an attempt to achieve an acceptable margin in a situation where the price of a product is determined externally by the market. This acceptable margin is achieved by identifying ways to reduce the costs of producing the product.

目标成本法的步骤:

1. 通过研究市场,确定产品的市场接受度,考虑市场份额;

Determine the price the market will accept for the product, based on market research. This may take into account the market share required.

2. 从价格中扣除必要的利润率,以得到目标成本;

Deduct a required profit margin from this price—this gives the target cost.

3. 预估产品的实际成本。如果是一个新产品,预估成本将是一个估价;

Estimate the actual cost of the product. If it is a new product, this will be an estimate.

4. 设法缩小产品的实际成本和目标成本差距 。

Identify ways to narrow the gap between the actual cost of the product and the target cost.

以上就是ACCA考试中关于目标成本法的相关解答,如需了解更多或想报名ACCA,欢迎点击下方按钮申请预评估,我们将有专业的辅导老师与您联系,为您提供全方位的注册、报考指导服务。

![]()

精品好课免费试听

查看被折叠的评论

被折叠评论包含相似、疑似不友好或无意义内容