In the Paper F6 (UK) exam, there will always be a minimum of five marks on inheritance tax. This two-part article will look at those aspects of inheritance tax that you need to know, with this first article explaining the scope of inheritance tax

The Paper F6 (UK) syllabus requires a basic understanding of inheritance tax (IHT), and this two-part article covers those aspects that you need to know. It is relevant to candidates taking Paper F6 (UK) in either June or December 2013, and is based on tax legislation as it applies to the tax year 2012–13 (Finance Act 2012).

There will always be a minimum of five marks (but no more than 15 marks) on IHT, with these marks being included in either Questions 3, 4 or 5.

The scope of inheritance tax IHT is paid on the value of a person’s estate when they die, but it also applies to certain lifetime transfers of assets. If IHT did not apply to lifetime transfers it would be very easy for a person to avoid tax by giving away all of their assets just before they died.

As far as Paper F6 (UK) is concerned the terms ‘transfer’ and ‘gift’ can be taken to mean the same thing. The person making a transfer is known as the donor, while the person receiving the transfer is known as the donee.

Unlike capital gains tax where, for example, a principal private residence is exempt, all of a person’s estate is generally chargeable to IHT.

A person who is domiciled in the UK is liable to IHT in respect of their worldwide assets. As far as Paper F6 (UK) is concerned, people will always be domiciled in the UK.

Transfers of value During a person’s lifetime IHT can only arise if a transfer of value is made. A transfer of value is defined as ‘any gratuitous disposition made by a person that results in a diminution in value of that person’s estate’. There are two important terms in this definition:

· Gratuitous: Poor business deals, for example, are not normally transfers of value because there is no gratuitous intent.

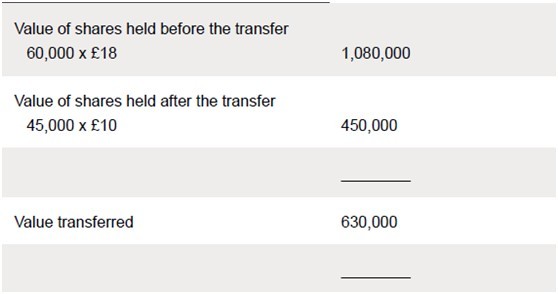

· Diminution in value: Normally there will be no difference between the diminution in value of the donor’s estate and the increase in value of the donee’s estate. However, in some cases it may be necessary to compare the value of the donor’s estate before the transfer, and the value after the transfer in order to compute the diminution in value. This will usually be the case where unquoted shares are concerned. Shares forming part of a controlling shareholding will be valued higher than shares forming part of a minority shareholding.

Example 1

On 4 May 2012 Daniel made a gift to his son of 15,000 £1 ordinary shares in ABC Ltd, an unquoted investment company. Before the transfer Daniel owned 60,000 shares out of ABC Ltd’s issued share capital of 100,000 £1 ordinary shares. ABC Ltd’s shares are worth £8 each for a holding of 15%, £10 each for a holding of 45%, and £18 each for a holding of 60%.

Although Daniel’s son received a 15% shareholding valued at £120,000 (15,000 x £8), Daniel’s transfer of value is calculated as follows:

By contrast, for capital gains tax purposes the valuation will be based on the market value of the shares gifted, which is £120,000.

As far as Paper F6 (UK) is concerned, a transfer of value will always be a gift of assets. A gift made during a person’s lifetime may be either potentially exempt or chargeable.

Potentially exempt transfers Any transfer that is made to another individual is a potentially exempt transfer (PET). A PET only becomes chargeable if the donor dies within seven years of making the gift. If the donor survives for seven years then the PET becomes exempt and can be completely ignored. Hence, such a transfer has the potential to be exempt.

If the donor dies within seven years of making a PET then it becomes chargeable. Tax will be charged according to the rates and allowances applicable to the tax year in which the donor dies. However, the value of a PET is fixed at the time that the gift is made.

Example 2

Sophie died on 23 January 2013. She had made the following lifetime gifts:

· 8 November 2005 – A gift of £450,000 to her son.

· 12 August 2010 – A gift of a house valued at £610,000 to her daughter. By 23 January 2013 the value of the house had increased to £655,000.

The gift to Sophie’s son on 8 November 2005 is a PET for £450,000. As it was made more than seven years before the date of Sophie’s death it is exempt from IHT.

The gift to Sophie’s daughter on 12 August 2010 is a PET for £610,000 and is initially ignored. It becomes chargeable as a result of Sophie dying within seven years of making the gift, and the transfer of £610,000 will be charged to IHT based on the rates and allowances for 2012–13.

Chargeable lifetime transfers

Any transfer that is made to a trust is a chargeable lifetime transfer (CLT).

There is no legal definition of what a trust is, but essentially a trust arises where a person transfers assets to people (the trustees) to hold for the benefit of other people (the beneficiaries). For example, parents may not want to make an outright gift of assets to their young children. Instead, assets can be put into a trust with the trust being controlled by trustees until the children are older.

Unlike a PET, a CLT is immediately charged to IHT based on the rates and allowances applicable to the tax year in which the CLT is made. An additional tax liability may then arise if the donor dies within seven years of making the gift. Just as for a PET, the value of a CLT is fixed at the time that the gift is made, but the additional tax liability is calculated using the rates and allowances applicable to the tax year in which the donor dies.

Example 3

Lim died on 4 December 2012. She had made the following lifetime gifts:

· 2 November 2005 – A gift of £420,000 to a trust.

· 21 August 2010 – A gift of a house valued at £615,000 to a trust. By 4 December 2012 the value of the house had increased to £650,000.

The gift to the trust on 2 November 2005 is a CLT for £420,000, and will be immediately charged to IHT based on the rates and allowances for 2005–06. There will be no additional tax liability as the gift was made more than seven years before the date of Lim’s death.

The gift to the trust on 21 August 2010 is a CLT for £615,000, and will be immediately charged to IHT based on the rates and allowances for 2010–11. Lim has died within seven years of making the gift so an additional tax liability may arise based on the rates and allowances for 2012–13.

精品好课免费试听