ELASTICITY

The concept of elasticity is concerned with the responsiveness of quantity demanded or quantity supplied to a change in price. If a small change in price brings about a

massive change in quantity demanded, the price elasticity of demand is said to be highly elastic. Conversely, if a change in price has little or no effect on the quantity demanded, the demand is said to be highly inelastic. This concept is obviously very important to producers, who have to estimate the potential effects of their pricing strategies over time. It is also important to government finance departments, which have to model the implications of imposing sales taxes on goods and services in order to predict tax revenues.

Price elasticity of demand is measured by dividing the change in quantity demanded by the change in price and, conversely, price elasticity of supply is measured by dividing the change in quantity supplied by the change in price. Price elasticity of demand occurs when an increase in price leads to a reduction in total revenue (p x q) between those two points on the demand curve, and price inelasticity occurs when an increase in price leads to an increase in total revenue. Unitary elasticity occurs when the change in price causes no change in total revenue.

In addition to price elasticity, there are similar concepts of relevance to your study:

· Income elasticity is the responsiveness of quantity demanded or supplied to a change in income.

· Cross elasticity is the responsiveness of quantity demanded or supplied of good X to a change in price of good Y.

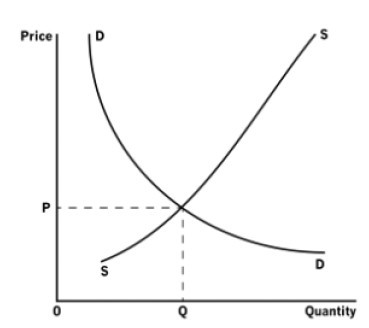

EQUILIBRIUM

Assuming all determinants of supply and demand are to be constant except price, a firm will produce where the supply curve intersects the demand curve. By definition, this is the point at which the quantity supplied equals the quantity demanded (Figure 3).

Price is determined at the intersection of the supply and demand curves.

If the price is set above the equilibrium price, this will result in the quantity supplied

exceeding the quantity demanded. Therefore, in order to clear its inventory, the company will need to reduce its price.

Conversely, if the price is set below the equilibrium price, this will result in an excess demand situation, and the only way to eliminate this is to increase the price. 、

MARKET INTERVENTION

In capitalist systems, allowing markets to operate freely is considered to be desirable, but it is generally accepted that market forces cannot be permitted to operate for all the goods and services required by society. Some goods and services are ‘public goods and services’, which means that they can only be provided adequately by intervention. These include law and order and the military. For this reason, the government or supra-national organisations may choose to introduce and maintain systems that will ensure that such goods and services are produced, and may fix prices either above or below the equilibrium price.

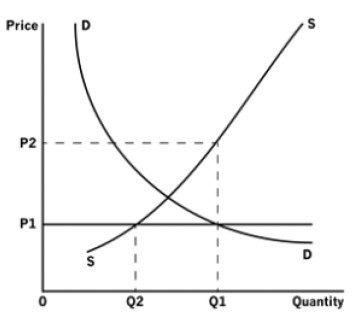

A maximum price is sometimes imposed in order to protect consumers. This will result in a situation in which the quantity demanded will exceed the quantity supplied, provided the maximum price is struck below the equilibrium price (Figure 4). There are numerous examples of this in real life. During World War 2, the UK government intervened in this way in order to ensure that families could obtain adequate supplies of goods such as bread, butter and petrol. One consequence of this is that there was excess demand in the system, and this led to an illegal market developing.

Figure 4: Maximum price

Maximum price is OP1. At this point, the quantity demanded (OQ1) exceeds quantity supplied (OQ2). The 'black market' price is OP2.

A minimum price is sometimes imposed in order to protect producers. Here, the quantity supplied will exceed the quantity demanded, provided the minimum price is struck at a level above the equilibrium price. One of the goals of the European Union

(EU) has been to protect the agricultural sector, and the common agricultural policy is a minimum price system. As a consequence of this, the agricultural sector of the EU has periodically generated surpluses.

The impact of intervention in the price system should not be seen as undesirable in all cases. However, one of the contributions that microeconomic analysis makes is that it teaches us that there will be consequences of such interventions, and society has to manage those consequences.

THEORY OF THE FIRM

The theory of the firm is a branch of microeconomics that examines the different ways in which firms within an industry may be structured, and seeks to derive lessons from these alternative structures.

Perfect competition

A perfectly competitive market is one in which:

· there are many firms producing homogeneous goods or services

· there are no barriers to entry to the market or exit from the market

· both producers and consumers have perfect knowledge of the market place.

Under such conditions, the price and level of output will always tend towards equilibrium as any producer that sets a price above equilibrium will not sell anything at all, and any producer that sets a price below equilibrium will obtain 100% market share. The demand ‘curve’ is perfectly elastic, which means that it will be horizontal.

As these conditions imply, there are few if any examples of perfectly competitive markets in real life. However, some financial markets approximate to this extreme model, and there is no doubt that in some fields of commerce the development of the internet as a trading platform has made the markets for some products, if not perfectly competitive, then certainly less imperfect.

Monopoly

A monopoly arises when there is only one producer in the market. It should be noted the laws of many countries define a monopoly in less extreme terms, usually referring to firms that have more than a specified share of a market.

Unlike perfect competition, monopolies can and do arise in real life. This may be because the producer has a statutory right to be the only producer, or the producer may be a corporation owned by the government itself.

A monopoly enjoys a privilege in that it can strike its own price in the market place, which can give rise to what economists call ‘super-normal profits’. For this reason, monopolies are usually subject to government control, or to regulation by non-governmental organisations.

Oligopoly

An oligopoly arises when there are few producers that exert considerable influence in

a market. As there are few producers, they are likely to have a high level of knowledge about the actions of their competitors, and should be able to predict responses to changes in their strategies.

The minimum number of firms in an oligopoly is two, and this particular form of oligopoly is called a duopoly. There are several examples of duopolies, including the two major cola producers and, for several product lines, Unilever and Procter & Gamble. However, markets dominated by perhaps up to six producers could be regarded as oligopolistic in nature. Where a few large producers dominate a market, the industry is said to be highly concentrated.

Although it is difficult to make generalisations across all oligopolistic markets, it is frequently noted that their characteristics include complex use of product differentiation, significant barriers to entry and a high level of influence on prices in the market place.

Monopolistic competition

Monopolistic competition arises in markets where there are many producers, but they will tend to use product differentiation to distinguish themselves from other producers in the market. Therefore, although their products may be very similar, their ability to differentiate means that they can act as monopolies in the short-run, irrespective of the actions of their competitors.

For monopolistic competition to exist, consumers must know of – or perceive – differences in products sold by firms. There tend to be fewer barriers to entry or exit than in oligopolistic markets.

CONCLUSIONS

Those embarking on their studies for Paper F1/FAB will quickly become aware that the syllabus is broad but shallow. It is essential to cover a wide range of topics, without necessarily having to study each component part in depth. The purpose of this article has therefore been to provide basic information on the most important areas of microeconomics without any intention of exploring any individual topic in detail. Awareness of key principles is important, but candidates should not assume that they have to be experts in order to deal with the objective test questions in the exam.

Written by a member of the Paper F1/FAB examining team

精品好课免费试听