by Tony Mock 21 May 2007 Stock control features in the syllabuses of several ACCA examination papers. The areas usually tested in these papers are:

· determining an economic order quantity (EOQ) – calculations to assess how many units of a particular stock item to order at a time

· finding an optimal re-order level (optimal ROL) – providing some idea of the level to which stocks can be allowed to fall before placing an order for more

· discussions of various practical aspects of stock management – often referred to by students with no practical experience as ‘theory’.

ADVANTAGES AND DISADVANTAGES OF HOLDING STOCK

The basis of the theoretical calculations of an EOQ and an optimal ROL is that there are advantages and disadvantages of holding stock (of buying stock in large or small quantities). The advantages include:

· the need to meet customer demand

· taking advantage of bulk discounts

· reducing total annual re-ordering cost

The disadvantages include:

· storage costs

· cost of capital tied up in stock

· deterioration, obsolescence, and theft

The aim behind the calculations of EOQ and ROL is to weigh up these, and other advantages and disadvantages and to find a suitable compromise level.

EOQ

When determining how much to order at a time, an organisation will recognise that:

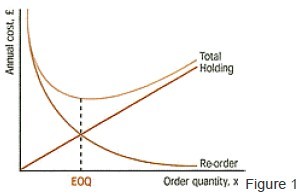

· as order quantity rises, average stock rises and the total annual cost of holding stock rises

· as order quantity rises, the number of orders decreases and the total annual re-order costs decrease.

The total of annual holding and re-order costs first decreases, then increases. The point at which cost is minimised is the EOQ. This cost behaviour is illustrated by the graph in Figure 1.

The way in which this EOQ is calculated is based on certain assumptions, including:

· constant purchase price

· constant demand and constant lead-time

· holding-cost dependent on average stock

· order costs independent of order quantity

The assumptions result in a pattern of stock that can be illustrated graphically as shown in Figure 2.

The Formula

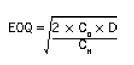

Using the standard ACCA notation in which:

CH = cost of holding a unit of stock for a year

CO = cost of placing an order

D = annual demand

also:

TOC = total annual re-ordering cost

THC = total annual holding cost

x = order quantity

then:

average stock = x/2

THC = x/2 × CH

and:

number of orders in a year = D/x

TOC = D/x × CO

The total annual cost (affected by order quantity) is:

C = THC + TOC = x/2 × CH + D/x × CO

This formula is not supplied in exams – it needs to be understood (and remembered).

The value of x, order quantity, that minimises this total cost is the EOQ, given by an easily remembered formula:

USE OF EOQ FORMULA

You need to take care over which figures you put into the formula, particularly in multiple-choice questions. The areas to beware of fall into two categories:

1. Relevant costs – only include those costs affected by order quantity. Only include those holding costs which (in total in a year) will double if you order twice as much at a time. Only include those order costs which (in total in a year) will double if you order twice as often. (Thus, fixed salaries to storekeepers or buying department staff will be excluded.)

2. Consistent units – ensure that figures inserted have consistent units. Annual demand and cost of holding a unit for a year. Both holding costs and re-ordering costs should be in £, or both in pence.

Page: 1 2 The original article>>

精品好课免费试听