SMA 1

Intro to strategic management accounting

01 Preview

Intro

.Strategic management accounting is defined as:

√Creating sustainable value by:

supporting the formation, selection, implementation and evaluation of organizational strategy

synthesizing information that captures financial and non-financial perspectives for both the internal and external environments, to enable effective resource allocation.

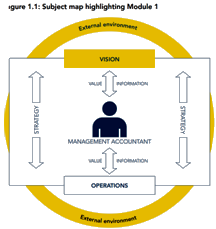

Subject map

.An organization decides on a strategic direction, where it believes value can be created. This value may be shareholder value, customer value or broader stakeholder value—depending on the type of organization involved.

.Creating value for organizations helps sell products and services, increases the share price, and ensures the future availability of capital to fund operations.

01 Part A: Value

Value

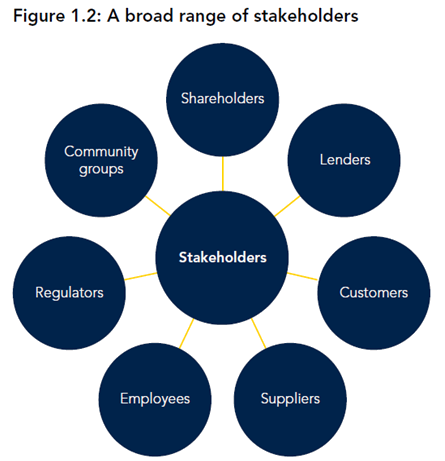

.Value is usually described as increasing shareholder wealth. However, this is both narrow and simplistic because it ignores other important and interested parties or stakeholders

.Each group has its own interests and desires and therefore its own definition of the ‘value’ it wishes to receive from an organization.

.Failure to consider stakeholder needs and desires will make it difficult to maintain and increase shareholder wealth.

.Value creation is just as relevant in the not-for-profit and public sectors.

.For example, national infrastructure, education, health and social welfare need to be managed just as effectively as privately run organizations.

.In the not-for-profit and public sectors, value is created for the members, citizens or residents (or taxpayers) of the nation, instead of wealth being increased for shareholders.

.Shareholder value

√The ultimate outcome for many organizations is to generate wealth for the owners. The owners have either started or invested in the organization to obtain appropriate returns for the risk involved. As such, many measures of value focus on shareholder value.

√However, pursuit of shareholder value while ignoring other areas of value creation is not sustainable. To ensure that an organization is able to create shareholder value over a prolonged period, its actions and use of resources need to be sustainable.

.Customer value

√The primary task for an organization is to create an output that has customer value.

√A key requirement is to produce this output at a cost that is lower than the price the customer is willing to pay, which leads to profitability and creates shareholder value

.Stakeholder value

√Shareholder wealth is a by-product of generating value in other areas. To create products or services, an organization will require community permission to operate, infrastructure, customers and employees—who will only supply their effort if the wages and conditions are adequate.

√So, consideration of stakeholders is critical to organizational success

.The viewpoint should be taken when deterring value

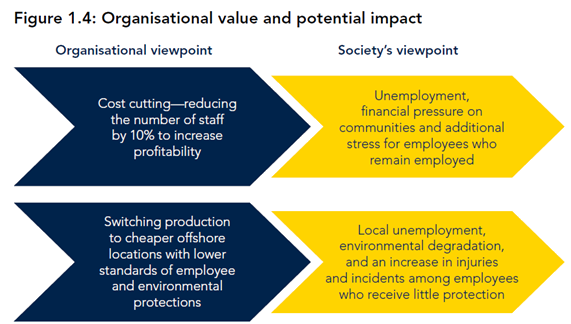

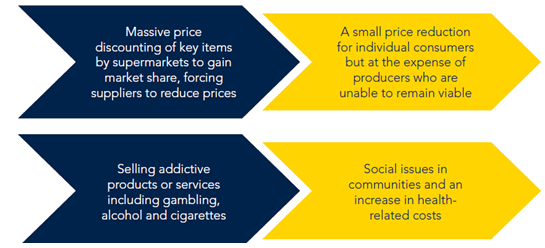

√The most obvious perspective is from the organization itself. Value is linked to the concept of ‘anything that is good for the business or organization’. However, other perspectives also exist, including that of society.

√The development of corporate social responsibility (CSR) indicates that people are interested in more than just the pure economic value that organizations create. They are also interested in ‘how’ that economic value is created, and they assess the impact of those actions (or inactions).

√CSR reporting has increased to help people understand the sustainable value or effect of an organization's activities from a social and environmental perspective

.Strategic management and strategic management accounting

√Strategic management describes the process by which an organization decides:

the direction it will take

the industry it will operate within

the types of products or services it will provide

its structure, systems and processes

its goals and objectives.

√Strategic management accounting aims to provide forward-looking information to assist management in decision-making.

√Unlike typical cost or/and management accounting, which focuses on internal accounting information, strategic management accounting evaluates external information—for example, trends in costs, prices, market share, competitors, suppliers and technologies—and their impacts on resources.

√Strategic management accounting uses a wide range of tools and techniques that support each stage of the strategic management process. So, strategic management accounting becomes an enabler, or a catalyst, that helps initiate and drive strategic management activity.

√Strategic management accounting helps organizations in their desire to create long-term, sustainable value that is of benefit to all stakeholders.

添加学习顾问

添加学习顾问